Student loans are an ordinary reality for many Canadians pursuing higher education. With the skyrocketing tuition, books, housing, and other expenses, student loans bridge the gap between savings, family support, scholarships, and total costs.

However, student loans come with real impacts on your financial life during school and beyond. Specifically, your credit history is tightly linked to how you manage student loans.

An Introduction to Student Loans in Canada

Let’s start with an overview of student loans in Canada. There are three main types of loans available:

- Federal student loans from the government’s Canada Student Loans Program

- Provincial student loans from your province’s financial aid program

- Private student loans from banks and other lenders

The terms, interest rates, eligibility criteria, and repayment options can vary widely between these types of loans. But they all share the common goal of helping students pay for the costs of post-secondary schooling when savings, family support, and scholarships fall short.

Student loans have become an unfortunate necessity for many to afford the continuously rising tuition fees, especially in fields like medicine and engineering. With prudent management, these loans can serve as investments into career-accelerating degrees. However, neglecting loan obligations can derail financial stability for years after graduation.

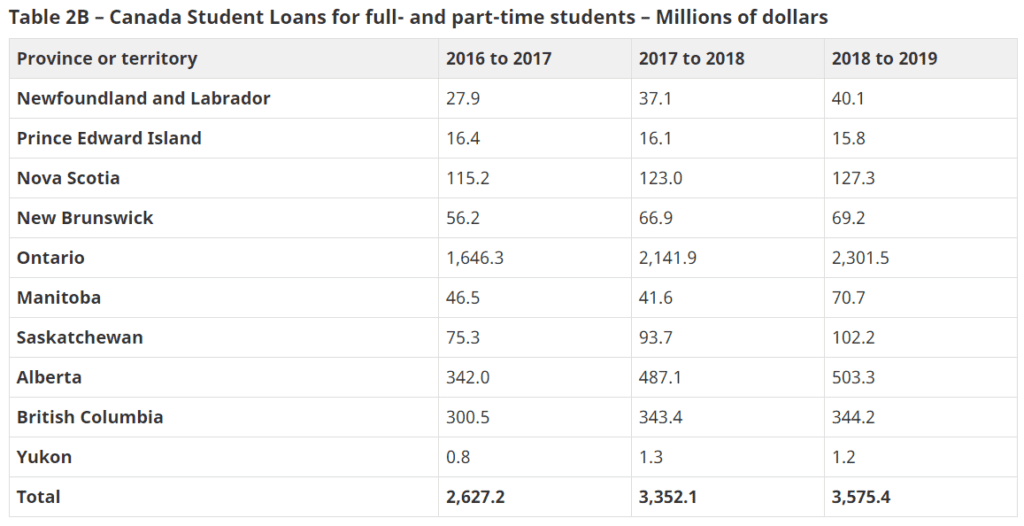

Key Differences in Provincial Student Loan Programs

One important facet of student loans in Canada is that each province and territory handles them slightly differently through their financial assistance programs.

For example, the province of Quebec has a distinct system called Aide financière aux études (AFE). The AFE provides Quebec residents with student loans and university or college education bursaries.

Compared to other provinces, Quebec has certain structural advantages:

- Relatively lower tuition fees at Quebec public universities and CEGEPs

- More financial aid per student from the provincial government

However, individual financial situations differ. Some students in Quebec may still need to borrow substantially more than the provincial aid offers to fund their education. This is where private student loans or lines of credit enter the picture.

Quebec provides almost $1 billion in loans and bursaries per year to over 175,000 students through AFE. Nearly 65% of Quebec post-secondary students utilize provincial aid.

Comparing Federal, Provincial and Private Student Loans

When it comes to types of student loans across Canada, there are several key contrasts:

- Federal loans have fixed interest rates set by the government, currently around 5-6% for Canada Student Loans.

- Provincial loans feature fixed and variable rate options, with 3-8% averages based on the province.

- Private loans offered by banks or credit unions involve higher variable interest rates, often indexed to the prime rate.

In general, interest rates on federal student loans are lower than provincial loans, which are lower than private lender loan rates. However, personal loans can provide supplementary funds when government aid packages fall short of the total costs.

Federal and provincial loans generally do not require payments while enrolled at least half-time in a degree program. Some private lenders offer similar in-school deferments, while others need interest payments during school.

The Vital Role of Credit Scores and Credit History

How do student loans connect to your credit scores and overall credit history? Well, credit scores influence nearly every aspect of borrowing, finances, and services you’ll need throughout life:

- Getting approved for loans, mortgages, and credit cards

- The interest rates you pay on debt

- Whether you meet income requirements for an apartment rental

- Your eligibility for cell phone plans and utility services

That’s why it’s so crucial to understand the link between student loan management and your credit history. Handling loans prudently while in school and continuing responsible payment after graduating significantly helps strengthen your credit profile for years to come.

Conversely, falling behind on student loan obligations or defaulting can seriously damage your credit standing in the long run. Missed payments or bankruptcy around student loans make future borrowing more difficult and expensive.

The Student Loan Payment History Factor in Credit Scoring

Your loan or credit card payment history is one of the most essential factors in generating credit scores. For student borrowers, this means:

- Making on-time monthly payments consistently improves your overall credit health. Lenders want to see reliability.

- Missing payments, even just once or twice, can rapidly damage your credit standing and lower your scores.

Establishing a track record of on-time payments throughout the loan repayment term goes a long way in building up your credit. Payment history commonly makes up 35% of credit calculations.

Conversely, relatively few missed or late payments can critically hurt your creditworthiness for years beyond just the student loan context. Keep this payment schedule disciplined with all your credit accounts.

Credit Utilization Ratios and Student Loan Debts

Another significant component of credit scores is your credit utilization – how much credit you have versus how much you owe. This ratio matters a lot.

The more student debt you carry, the higher your overall credit utilization. Even with on-time payments, high student loan balances make lenders consider you riskier to take on new loans, cards, or products after graduation.

Past student loans weigh indirectly on your ability to access new credit down the road, negatively impacting this utilization ratio in your profile. Keeping this ratio low is critical for new borrowing and refinancing pre-existing debts.

For example, experts recommend keeping utilization below 30%. This means maintaining at least $3 of available credit for every $1 owed. It is difficult with hefty uninsured student debts, but it is possible.

Interest Rates: A Double-Edged Sword for Credit Scores

Student loans universally involve interest costs, whether during school or after graduation. Let’s examine how rates impact credit scores:

- Federal loan rates are fixed around 5-6% for Canada Student Loans, regardless of credit.

- Provincial loan rates include fixed (3-5%) and variable (prime + 1-3%) options.

- Private loan rates are higher as they track the prime rate plus an added percent.

Student loan interest affects your credit in two key ways:

- It steadily increases the total debt you owe over time through capitalization.

- It inflates your debt-to-income ratios after school by raising monthly burdens.

Yet there is a positive angle, too. Diligently paying interest costs each month displays fiscal responsibility. Knocking down interest first shows lenders your ability to handle debts in a prioritized manner.

The key takeaway? Interest exacerbates loans impacting credit but is manageable. Never ignore interest costs, as capitalization snowballs fast.

The Controversy of Refinancing Your Student Loans

Some student borrowers consider refinancing as a post-graduation strategy to improve repayment terms. This debt consolidation approach involves taking out a new and larger private loan to pay off your existing federal and provincial student loans.

Two potential benefits include:

- Securing a lower fixed interest rate on the refinanced amount

- Reducing your monthly payments by extending the repayment term

However, refinancing also carries risks:

- It may significantly extend the total repayment timeline—more interest over time.

- You’ll undergo a hard credit check, causing a small temporary score drop.

- Loss of federal loan protections like income-based repayment and forgiveness.

Overall, evaluate refinancing carefully based on your financial situation and career prospects. Refinancing helps some former students but costs others more interest charges over the entire repayment period.

Expert Tips for Responsibly Managing Student Debt

Here are proven best practices for managing student loans to maintain good credit standing:

- Make all monthly payments on time every single month. Set up autopay.

- Actively track your interest rates and capitalization amounts. Don’t let interest snowball.

- Make lump sum payments whenever possible to directly reduce your high-interest principal.

- Increase your payment if it is affordable to pay down the loan balances faster.

- Look into income-based repayment plans or extended terms to lower required payments.

- Consider refinancing intelligently if the benefits outweigh the costs for your situation.

- Maintain good overall credit habits – pay all bills on time and keep credit card and other debts low.

- Start building credit early with a student card, using it lightly, and paying it off monthly.

Having Student Loan Payment Troubles? BHM Financial Can Help

As we’ve explored, student loans can negatively impact your credit if you miss payments or default. Yet financial hurdles happen. Assistance is available if you’re struggling to keep up with student loan bills due to job loss, medical expenses, or other emergencies.

Traditional banks often turn away borrowers facing credit challenges. But viable alternatives exist, like BHM Financial Group – a leading provider of asset-based loans tailored for Canadians with past credit difficulties.

Since 2005, BHM Financial has specialized in creating customized loan packages based on a client’s current assets and income stability, not outdated credit scores. Their experts evaluate your complete financial picture to structure responsible loan solutions at reasonable rates.

If your student loans are dragging down your credit or you need to consolidate debts at a lower interest cost, contact BHM Financial for a free consultation. Discover the power of asset-based lending and get expert guidance on options to take control of your finances. Don’t let student loans wreck your credit future.

Conclusion: Student Loan Impacts on Credit Histories

In summary, student loans are a common avenue for financing higher education pursuits for Canadian students. With tuition costs continuing to outpace inflation, borrowing requirements will only expand. That’s why it’s essential to understand the potential impacts of student loans on your credit history and scores.

Acting responsibly to manage student loan obligations helps strengthen your credit health over time rather than weaken it. Avoiding missed payments, retaining control of interest costs, keeping utilization down, and preventing default ensures student borrowing aids your financial foundations rather than harms them.

While challenging, students can take proactive steps and use borrowing prudently as leverage to build their assets, earnings potential, and credit capabilities for the future. With loans playing such a key role, educating yourself on minimizing their credit impacts is critical.