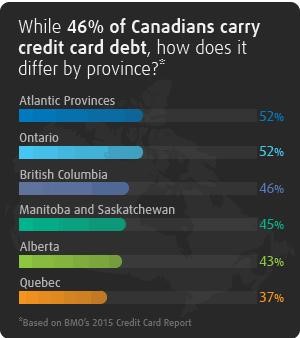

When it comes to negotiating credit card debt, it may seem a little petrifying. However, through the right set of coherent and proficient negotiation ideas, one can successfully work his way out of the debt. There is now a noticeable trend of credit card debt in Canada, as in an article on Debt and Family type in Canada. The results suggest a high debt to asset ratio, and the debt is not sufficiently supported by the assets (Hurst, 2011). It is no surprise that the burden of debt can be mentally exhausting. This statement can be corroborated by the research conducted by Keeze & Schmitz (2012), which revealed that individuals who are indebted to a large sum of money face severe health issues (p. 534). Fittingly offloading your debt is the only gateway towards reducing the un-called for stress.

To negotiate effectively, one should always strategize and organize the options available in advance. The individual should make up his mind to go about his plan, whether he wants to negotiate personally or with companies’ help.

In this article

Hardship Plan / Forbearance Program

Insight On Interest Capitalization

Getting External Help

Every individual has its own set of strengths. Everyone does not need to have the ability to carry out negotiations effectively. Some individuals can also face a hard time dealing with financial stress and cannot focus on anything else, even the solutions. If robust negotiations regarding debt settlement do not seem to be your teacup, you can always seek help from the professionals. Some companies can help in steering the right kind of debt settlement for you.

Credit Counseling Companies

Credit Counseling Companies will negotiate with your creditors on your behalf. These agencies use a diverse set of tools to get you out of your credit debt gradually. Some of these companies can be non-profit at times. However, most of them are for-profit organizations and will most likely charge a high fee for their services. These agencies can operate in distinct ways. Some offer face to face counseling, while some also provide their services through emails or calls. By getting help from such agencies is often useful in getting unexpected help. These agencies will broaden your horizons regarding options available for you and prevent you from declaring bankruptcy. After discussing the details of your debt, the company will contact your creditor and offer a somewhat reasonable debt payment plan.

Moreover, the pressure of negotiating with creditors can be very nerve-wracking for some; having the professionals take in charge will automatically lessen the stress in that regard. Such agencies can assist you in arranging an effective debt management plan for you. After discussing suitable options for possible debt settlement and debt consolidation services, they will communicate with your creditors and eventually help you get debt-free.

Debt Settlement Companies

Debt Settlement Companies are mostly for-profit organizations. These companies work towards settling debts or altering the terms for debt payment on behalf of the debtor. In this scenario, you cease making payments to your creditor instead of paying it to build your account. Once your account is big enough, the company will contact your credit card issuer and negotiate to settle your debt. Having experienced professionals strategize your debt payment options will save your time and help you get out of debt more conveniently. In addition to that, a debt settlement company can also enhance your knowledge regarding financial literacy.

Know Your Risks

While getting help from the professionals can seem like a desirable option, you should also be aware of the risks involved while working with debt settlement companies. First and foremost, before considering getting help from these companies, you should also be mindful that they charge a high amount for their services. Moreover, providing debt settlement services can sometimes put you in a negative light and can hinder your ability to get credit in the future. It is also commonly known that the debt settlement company usually asks you to make payments in a specific bank account, and you might have to pay extra to use that account.

Occasionally, some companies may fail to make desirable arrangements for you, or your creditors may simply deny cooperating with individual companies. Lastly, you should avoid getting help from companies that ask you to completely block out all communication with your creditors or charge you for their services before settling your debts. As per the Federal Trade Commission 2020, for-profit debt settlement companies cannot charge their clients with fees until and unless they are successful in settling the client’s debts (Prater, 2010).

Trust Yourself

You can always get external help but might end up paying thousands of dollars to these companies. Fortunately, there is still an option of negotiating yourself. This way, you can save a ton of money and also avoid scams.

It is okay to feel a little overwhelmed about getting on the phone with your creditor. Taking into account the points mentioned below can help you negotiate confidently and, without doubt, save a great deal of inconvenience for both the parties:

You should be informed about the exact amount that you are indebted to and how much you earn. Such a strategy will help you negotiate confidently and sensibly.

You should have all the necessary documents in front of you since this will likely. Having the papers laid out in front of you saves time and makes your responses prompt and accurate.

You must go through every detail of the documents in advance. It is wise to go through and understand every little detail of the papers as it helps in the decision-making process regarding a suitable debt settlement option.

Put more effort!

You should determine the best rate or best settlement option suitable for you beforehand. Educating yourself regarding potential benefits and the risks involved with your prospects will prepare you even for the worst.

You should drive a hard bargain during the negotiation. Settling on bank’s terms can be tricky and not necessarily in your best interest. Knowing what’s doable for you is very important. You don’t want to keep on deteriorating your credit score.

You should always ensure to get the agreement in writing. Once you are successful in convincing your creditor for a suitable settlement strategy, obtain the terms of the deal in a written document form. This will serve as secure evidence for you in the future.

You should also keep a pen and a notebook to jot down all the essential information conveyed during the meeting. It is impossible to retain all the details communicated during the discussion. Therefore, you should be proficient enough to keep noting down all the necessary information that you think is relevant to your debt situation.

Do not be afraid; you have what it takes; you just need to trust yourself. Constant calls from your creditor demanding the payment can make you nervous, which is understandable. However, you should always remember that businesses are all based on good negotiations. Your creditor needs his money, and you are only trying to make that happen.

Debt Settlement Options

Educating yourself concerning ‘credit card debt settlement options’ is of prime importance. It makes you aware of the different choices available for you, and which one of these choices suits you the most. You get to gain knowledge about debt adjustment which, in turn, enables you to make informed, conscious decisions. It gives you the confidence to appropriately deal with your creditor and simultaneously maintain a healthy relationship.

These are the five basic types of debt settlements that your creditor is most likely to accept:

- Lump-sum Settlement

- Workout Agreement

- Hardship Plan / Forbearance Program

- Debt Management Program

- Debt Settlement Program

Lump-sum Settlement

A lump-sum settlement is considered one of the most beneficial ways out of the five possibilities mentioned above. This type of arrangement involves you paying off the debt in one large payment. For instance, if you owe your creditor $5000 and $1500 of your debt includes late fee or interest, you can negotiate with your creditor to accept your payment of the initial amount of $3500. Before making your offer, make sure you have access to the money and can commit to your word. When your creditor accepts your offer, ensure that you have the acceptance of the lump sum settlement in a document form. However, you should also be aware that you may receive a 1099-C tax notice, which will require you to pay the additional tax amount on the remaining $1500 in next year’s income (Williams & Rafter, 2020). One possible drawback of choosing this settlement is that your inability to pay back your debt can reflect poorly on your credit score.

Workout Agreement

The second-best choice for debt settlement has to be the workout agreement. Under the workout agreement, your creditor might settle on lower interest rates, minimize your late fee charges or even agree to forgo of the interest payments entirely but only temporarily. You can also appeal to the bank to let go of your previous late fees. However, it will always be the bank’s decision to grant you the stated favor. Regardless, your credit card issuer is most likely to shut down your credit line under the workout agreement. This will have a gloomy impact on your credit score and increase your credit utilization rate.

Credit utilization rate is concerned with the ratio that banks or other lenders use to ascertain the worth of your credit. And, the lower the credit utilization, the better it is for your credit score. For example, if your account had an amount of $3000 present in it already, it will increase your credit utilization rate, which will, in turn, damage your credit score. The figure below further explains how the credit utilization rate operates.

Hardship Plan / Forbearance Program

Choosing the hardship plan, often referred to as the forbearance program, can be a suitable option if your financial complications are temporary. Temporary financial setbacks can include medical emergencies, unplanned employment, a sudden increase in the cost of rent, a reduction in wages, etc. In such cases, you can request your creditor for a forbearance program if they offer one. With the help of the hardship plan, your interest and late fee can be minimized. Your creditor can also agree to let you skip payments temporarily until you are capable enough to pull through your financial problems. Again, just like the other two types of settlement, a hardship plan can also negatively affect your credit history and credit score. This will sequentially act as an obstacle in your future credit availability options.

Debt Management Program

This option is desirable for you if you do not wish to negotiate with your creditor yourself. Under this program, you will need to connect to a credit counseling company. The counselor will set up a meeting with you and discuss the best options to free you from your debts. After deciding the appropriate debt payment plan, he will make an offer to your creditor on your behalf. He can help you lower your interest payments or minimize late fee obligations according to your financial conditions. However, this will close all your accounts and increase the credit utilization rate. Below are the five critical factors that affect your credit score; credit utilization level alone takes up 30% of the credit score.

Debt Settlement Program

You can go about this program either by yourself or with the assistance of debt settlement companies. This type of settlement requires you to stop your payments to your creditor for a month until your credit card issuer agrees to accept a more affordable amount from your side. On the other hand, even if you are fortunate enough to succeed in this strategy, your credit history is most likely to suffer. The debt settle program should only be considered when all other alternatives have failed.

Insight On Interest Capitalization

When you are already indebted to pay a large sum of money to your creditor, interest, and capitalization can only make the situation worse. However, a comprehensive understanding of these two components can help you steer clear of the additional burden.

Interest is the amount generated on the amount borrowed. It is calculated as a certain percentage of loans paid to the lender with the original amount (mostly called the principal). This borrowing cost depends upon factors you will be required to pay a substantial amount of interest in cases of high-interest rates when you borrow a large amount and are granted more extended periods to pay back your loan.

Failure of interest payments results in capitalization. The amount can then be referred to as capitalized interest and is added to the principal amount. In other words, failure to pay interest would result in you paying interest on your interest.

Avoiding capitalization is essential because it can help you save thousands of dollars. To prevent interest capitalization, you can pay off the interest-only amount to the lender before the loan payment period. However, this is only possible if you have the means to do so. Otherwise, you can eliminate your interest payment by paying it off as soon as it accrues, this will ensure that there is no interest left to be capitalized. You can also utilize the grace period to pay off your interest. Grace period refers to the period shortly after the payment deadline that usually lasts six months, in which payment can still be made without any sort of penalization.

Conclusion

Lastly, if you have approved your appeal for forbearance program or hardship plan, you can temporarily skip payments until your financial situation improves. However, this is only useful for a short term fix as the interest keeps on building up even during the majority of forbearance periods. It is also possible that when the forbearance period ends, the interest will resume its capitalization process.

It is always advisable to pay off the interest on time to avoid capitalization altogether. Capitalization only adds to your burden, and you end up paying the magnified amount of money, three quarters of which you could not even pay in the first place. By making interest payments your top priority, you can save yourself a lot of money and mental torture.

References

Hurst, M. (2011). Debt and family type in Canada. Canadian Social Trends, 91, 40-47.

Keese, M., & Schmitz, H. (2012). Broke, Ill, and Obese: Is There an Effect of Household Debt on Health? Review of Income and Wealth, 60(3), 525–541.

Prater, C. (2010, July 29). FTC bans upfront fees for debt settlement firms. Retrieved August 07, 2020, from https://creditcards.com/credit-card-news/ftc-debt-settlement-rules-1282/

Williams, F. O., & Rafter, D. (2020, March 03). 1099-C surprise: Canceled debt often taxable as income. Retrieved August 07, 2020, from https://www.creditcards.com/credit-card-news/forgiven-debt-1099c-income-tax-3513/